Qualify for Fha Again After 5 Years

What Is an FHA Loan?

"FHA loans" are mortgages insured by the Federal Housing Administration (FHA), which tin exist issued by whatsoever FHA-approved lender in the United States.

Congress established the FHA in 1934 to help lower income borrowers obtain a mortgage who otherwise would accept trouble qualifying. In 1965, the FHA became office of the Department of Housing and Urban Development's (HUD) Office of Housing.

Before the FHA was created, it was common for homeowners to put down a staggering fifty% of the value of the property equally a down payment on short-term balloon mortgages, which clearly wasn't practical going forward.

Jump to FHA loan topics:

– FHA Loan Requirements

– FHA Mortgage Rates

– Types of FHA Loans

– Do FHA Loans Require Mortgage Insurance?

– FHA Loan Credit Score Requirements

– Are DACA recipients eligible?

Unlike conventional dwelling house loans, FHA loans are government-backed, which protects lenders against defaults, making it possible to for them to offer prospective borrowers more competitive involvement rates on traditionally more risky loans.

An FHA home loan works like any other mortgage in that you infringe a certain amount of coin from a lender and pay it back, typically over 30 years via fixed mortgages.

The main stardom is that FHA loans accuse both upfront and monthly mortgage insurance premiums, often for the life of the loan.

Notwithstanding, they also come up with low down payment and credit score requirements, making them one of the easier home loans to qualify for. Oh, and FHA interest rates are some of the lowest around!

Let's explore some of the finer details to give you a amend agreement of these common loans to run across if ane is correct for yous.

FHA Loan Requirements

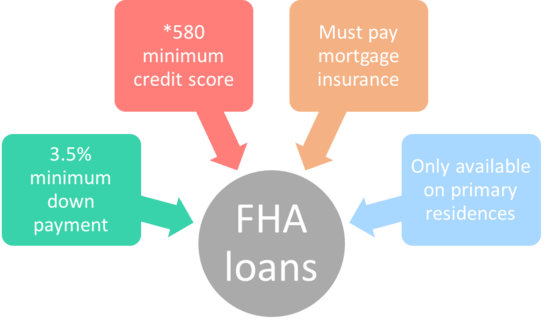

Because FHA loans are insured by the authorities, they have easier credit qualifying guidelines than most other loans, besides as relatively low closing costs and down payment requirements.

What is the minimum downwardly payment on an FHA loan?

Wondering how much do yous need down for an FHA loan? Your down payment tin can be as low as three.5% of the purchase price, assuming you accept at least a 580 credit score. And closing costs can be bundled with the loan. In other words, you don't need much greenbacks to close.

In fact, gift funds can be used for 100% of the borrower's endmost costs and down payment, making them a truly affordable choice for an individual with picayune cash on hand. Still, y'all cannot use a credit menu or unsecured loan to fund the downward payment or closing costs.

Y'all tin get an FHA loan with zero downward?

Technically no, y'all still need to provide 3.5% down. But if the 3.v% is gifted past an acceptable donor, it's effectively cipher down for the borrower.

For a rate and term refinance, you can go a loan-to-value (LTV) as high as 97.75% of the appraised value (plus the upfront mortgage insurance premium.)

All the same, information technology'south important to note that while the FHA has relatively lax guidelines for its loans, individual banks and lenders will ever fix their own FHA underwriting guidelines on top of those, known as lender overlays.

And continue in mind that the FHA doesn't actually lend money to borrowers, nor does the bureau set the interest rates on FHA loans, information technology simply insures the loans.

What is the max loan amount for an FHA loan?

The max loan corporeality (national loan limit ceiling) for FHA loans for one-unit properties is $970,800, with the exception of some Hawaiian counties that go as high as $i,456,200.

Additionally, the loan limits are college for 2-four unit of measurement properties nationwide.

However, many counties, even large metros, accept loan limits at or very close to the national floor, which is set up at a much lower $420,680.

For instance, Phoenix, Arizona merely allows FHA loan amounts upwards to $441,600 because home prices aren't equally high there.

There are other counties that have a max loan corporeality in between the floor and ceiling, such every bit San Diego, CA, where the max is gear up at $879,750.

The same goes for Miami ($460,000), though it's not much higher than the national floor.

In other words, you actually gotta cheque your county before bold your loan amount will work with the FHA.

What are the 2022 FHA loan limits?

In 2022, the max loan amount in high-toll areas will increase to $970,800 from $822,375, while the floor in lower-cost areas will rise to $420,680 from $356,362.

Loan amounts above the ceiling are considered jumbo loans, and thus are not eligible for FHA financing.

What are the FHA loan income requirements?

Despite some misconceptions, there is no minimum or maximum income required for an FHA loan. This means both depression-income and wealthy home buyers tin have reward of the plan if they so choose.

However, there are DTI limits that the applicant must abide past, like any other mortgage, though the FHA is relatively liberal in this department.

It should be noted that some state housing finance agencies do have income limits for their own FHA-based loan programs.

Do I need to be a first-time home buyer to get an FHA loan?

Nope. The program can exist used by both kickoff-time home buyers and repeat buyers, but it'south definitely more than popular with the former considering it's geared toward individuals with limited down payment funds.

For instance, move-up buyers probably won't use an FHA loan because the gain from their existing home sale tin can be used equally a downwardly payment on their new property.

And there are some limitations in terms of how many FHA loans yous tin can accept, which I explicate in particular below.

Do y'all need reserves for an FHA loan?

No, reserves are not required on FHA loans if it's a 1-2 unit belongings. For 3-four unit of measurement properties, you'll need iii months of PITI payments. And the reserves cannot be gifted nor can they exist gain from the transaction.

What banks do FHA home loans?

If yous're wondering how to get an FHA loan, pretty much any banking company or lender (or mortgage broker) that originates mortgages will besides offering FHA loans.

While the FHA insures these loans on behalf of the authorities, individual companies like Rocket Mortgage and Wells Fargo are the ones that really make them.

My estimate is that more than ix out of 10 lenders offering them, then you should accept no trouble finding a participating lender. Check out my list of the acme FHA lenders.

Who are the all-time FHA loan lenders?

The best FHA lender is the one who can competently close your loan and do so without charging you a lot of money, or giving you lot a higher-than-marketplace rate.

At that place is no one lender that is meliorate than the rest all of the time. Results will vary based on your loan scenario and who you happen to work with. Your feel can even differ within the aforementioned bank among different employees.

FHA Mortgage Rates Are Generally the Lowest Available

One of the biggest draws of FHA loans is the depression mortgage rates. They happen to be some of the most competitive effectually, though yous exercise have to consider the fact that yous'll take to pay mortgage insurance. That will plain increase your overall housing payment.

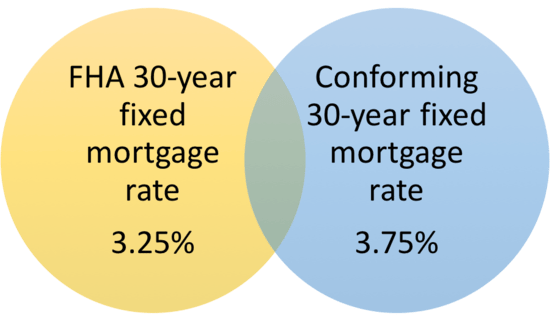

In general, you might find that a xxx-year fixed FHA mortgage charge per unit is priced nearly 0.25% to 0.50% below a comparable conforming loan (those backed past Fannie Mae and Freddie Mac).

And so if the not-FHA loan mortgage charge per unit is 3.75%, the FHA mortgage rate could be as low every bit 3.25%. Of course, it depends on the lender. The difference could be every bit little every bit an .125% or a .25% as well.

This interest charge per unit advantage makes FHA loans competitive, even if y'all have to pay both upfront and monthly mortgage insurance (often for the life of the loan!).

The depression rate also makes it easier to qualify for an FHA loan, every bit any reduction in monthly payment could be but enough to become your DTI to where it needs to exist.

Only if you compare the April of an FHA loan to a befitting loan, you lot might detect that information technology's higher. This explains why many individuals refinance out of the FHA once they accept sufficient equity to exercise so.

Types of FHA Loans

- You can get a fixed-rate habitation loan or an ARM

- Though virtually borrowers go with a 30-year fixed

- Typically used as home purchase loans

- But their streamline refinance program is likewise popular

The FHA has a variety of loan programs geared toward first-time home buyers, along with contrary mortgages for senior citizens, and has insured more than 34 1000000 mortgages since inception.

FHA loans are available for both purchases and refinances, including cash out refinances.

The max LTV for a cash-out FHA loan is a relatively depression 80% ( instituted in September 2019), downward from 85% mail-crisis (instituted in 2009) and an even higher 95% before the mortgage crisis took place.

Information technology should besides be noted that mortgages with fewer than six months of payment history are non eligible for an FHA cash out refinance.

And the borrower must have made all mortgage payments on time in the preceding six to 12 months to be eligible.

For those with existing FHA loans looking to refinance to another FHA loan, the streamline refinance program is a quick and piece of cake option that provides a ton of flexibility, even for those who lack habitation equity.

Does the FHA offering ARM loans?

Yes, FHA loans can be either adjustable-charge per unit mortgages or fixed-charge per unit mortgages. The FHA 30-year stock-still loan is certainly the most common.

However, many FHA lenders offer both a v/1 ARM and a 3/1 ARM. If the interest rate is adaptable, it will be based on the one-Year Abiding Maturity Treasury Alphabetize, which is the most widely used mortgage index.

Does the FHA offering 15-year loans?

Absolutely! You can get a variety of unlike stock-still-charge per unit FHA products, including a 15-year fixed from nigh lenders, though the college monthly payments would probably serve as a barrier to most offset-time home buyers. Some may even offering a 10-yr fixed production, a twenty-year stock-still, or even a 25-year fixed.

Tin I get a 2nd mortgage backside an FHA loan?

Information technology'due south possible, though well-nigh FHA loans take very loftier LTV ratios, and almost home equity loans limit the CLTV (combined LTV) to effectually 85%-95%, and so you'll need some disinterestedness before taking out a second mortgage such as a HELOC.

A second mortgage may also come into play when getting downwards payment aid during a home purchase, whereby the loan is subordinate to the FHA loan.

Does FHA practise construction loans?

Yeah. They have a construction plan called a 203k loan that allows FHA borrowers to renovate their homes while too financing the purchase at the same fourth dimension.

Fun fact – the standard FHA loan program is technically known equally the "FHA 203b" in instance you're wondering where that name comes from.

Can FHA loans be used on two-4 unit properties?

FHA loans can be used to finance one-4 unit residential properties, including condominiums, manufactured homes and mobile homes (provided it is on a permanent foundation), along with multifamily properties.

Notwithstanding, FHA loans are generally simply reserved for borrowers who intend to occupy their properties.

Does FHA have to be owner occupied?

Aye, the holding yous are purchasing with an FHA loan has to be owner-occupied, meaning you lot intend to live in it shortly after purchase (within 60 days of endmost). You are too expected to live in it for at least a twelvemonth. Nonetheless, that doesn't mean y'all can't eventually plow your primary residence into a rental.

Tin FHA financing be used for an investment belongings?

The FHA's single family unit loan program is limited to owner-occupied master residences but, meaning investment backdrop aren't eligible. But every bit noted above, 1-4 units are permitted and those additional units tin can be rented out if you occupy one of the other units. And it may be possible to rent the holding in the future.

Tin can you rent out a business firm with an FHA loan?

Generally, aye, but the FHA requires a borrower to constitute "bona fide occupancy" within 60 days of closing and continued occupancy for at least one twelvemonth. Subsequently that time, it's basically off-white game to rent it out though the FHA does say information technology will non insure a mortgage if information technology'due south determined that the loan was used as a vehicle for obtaining investment properties.

Can I take more than than i FHA loan?

Tip: Technically, you may only agree one FHA loan at any given time. The FHA limits the number of FHA loans borrowers may possess to reduce the chances of default, and because the program isn't geared toward investors.

For example, they don't want one individual to purchase multiple investment properties all financed by the FHA, as it would put more than adventure on the agency. Just at that place are certain exceptions that allow borrowers to hold more than than one FHA loan.

Tin can I get an FHA loan on a second abode?

A co-borrower with an FHA loan may be able to become some other FHA loan if going through a divorce, and a borrower who outgrows their existing home may be able to get another FHA loan on a larger dwelling, and maintain the old FHA loan on what would go their investment property.

Information technology's too possible to get a second FHA loan if relocating for work, whereby you purchase a second property as a primary residence and continue the old property equally well.

Lastly, if you are a not-occupying co-borrower on an existing FHA loan, information technology'south possible to get another FHA loan for a property yous intend to occupy.

But y'all'll need to provide supporting evidence in gild for it to piece of work.

Can I get an FHA loan if I already own a abode?

Yes, but you might see some roadblocks if your existing dwelling house has FHA financing, every bit noted above.

If your existing home is free and clear or financed with a non-FHA mortgage, you should exist good to go as long equally the subject belongings volition be your main residence.

Do FHA Loans Require Mortgage Insurance?

- FHA loans impose both an upfront and annual insurance premium

- Which is one of the downsides to FHA financing

- And it can't be avoided anymore regardless of loan type or down payment

- Nor tin can information technology exist cancelled in most cases

One downside to FHA loans as opposed to conventional mortgages is that the borrower must pay mortgage insurance both upfront and annually, regardless of the LTV ratio.

This differs from privately insured mortgages, which merely require mortgage insurance if the LTV is greater than 80%.

The upfront mortgage insurance premium:

FHA loans accept a hefty upfront mortgage insurance premium equal to 1.75% of the loan amount. This is typically arranged into the loan amount and paid off throughout the life of the loan.

For instance, if y'all were to buy a $100,000 property and put down the minimum 3.5%, you'd be subject to an upfront MIP of $1,688.75, which would be added to the $96,500 base of operations loan amount, creating a total loan amount of $98,188.75.

And no, the upfront MIP is not rounded up to the nearest dollar. Employ a mortgage calculator to figure out the premium and final loan amount.

Nonetheless, your LTV would still exist considered 96.5%, despite the addition of the upfront MIP.

The almanac mortgage insurance premium:

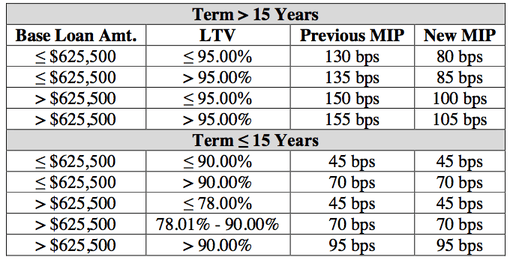

Merely wait, in that location's more! Y'all must also pay an annual mortgage insurance premium (paid monthly) if you take out an FHA loan, which varies based on the attributes of the loan.

Showtime January 26th, 2015, if the loan-to-value is less than or equal to 95%, you will accept to pay an annual mortgage insurance premium of 0.80% of the loan amount. For FHA loans with an LTV higher up 95%, the annual insurance premium is 0.85%. And it'south even higher if the loan amount exceeds $625,500.

For loan terms of 15 years or shorter, the annual mortgage insurance premiums are significantly lower (see charts above).

Additionally, how long you pay the annual MIP depends on the LTV of the loan at the time of origination.

How practice you calculate the almanac MIP on an FHA loan?

To calculate the annual MIP, you use the annual average outstanding loan balance based on the original acquittal schedule. An easy way to ballpark the cost is to simply multiply the loan amount by the MIP rate and divide past 12.

For case, a $200,000 loan corporeality multiplied by 0.0085% equals $1,700. That's $141.67 per month that is added to the base mortgage payment.

In year ii, it is recalculated and will go downward slightly because the average outstanding loan balance will be lower.

And every 12 months thereafter the price of the MIP will get downwardly equally the loan residue is reduced (a mortgage figurer may help hither).

However, paying down the loan balance early on does not affect the MIP calculation because it'southward based on the original amortization regardless of any extra payments you may make.

Notation: The FHA has increased mortgage insurance premiums several times as a result of college default rates, and borrowers should not be surprised if premiums ascent again in the future.

Do FHA Loans Have Prepayment Penalties?

- They do not have prepayment penalties

- Only in that location is a caveat

- Depending on when you lot pay off your FHA loan

- You lot may pay a total month's interest

The adept news is FHA practise Not take prepayment penalties, meaning you lot can pay off your FHA loan whenever yous feel similar it without being assessed a penalty.

Prepayment penalties aren't very common these days, though they were quite prevalent on conventional loans during the housing blast in the early 2000s.

There is a caveat…

All the same, there is 1 thing you should sentry out for. Though FHA loans don't permit for prepayment penalties, you may be required to pay the total month's involvement in which you refinance or pay off your loan because the FHA requires total-month interest payoffs.

In other words, if yous refinance your FHA loan on Jan 10th, you lot might have to pay interest for the remaining 21 days, even if the loan is technically "paid off."

It'due south kind of a backdoor prepay penalty, and one that volition probably be revised (removed) soon for futurity FHA borrowers. If yous're a electric current FHA loan holder, you may want to sell or refinance at the terminate of the calendar month to avoid this extra involvement expense.

Update: As expected, they eliminated the collection of post-settlement involvement. For FHA loans closed on or after January 21st, 2015, interest volition only be nerveless through the date the loan closes, as opposed to the cease of the calendar month. Legacy loans will yet be affected by the one-time policy if/when they are paid off early.

Are FHA Loans Assumable?

- An FHA loan tin be assumed

- Which is i benefit to having one

- But how oft this option is actually exercised is unclear

- My guess is that it doesn't happen frequently

Another benefit to FHA loans is that they are assumable, meaning someone with an FHA loan can laissez passer it on to you if the interest rate is favorable relative to electric current market place rates.

For example, if someone took out an FHA loan at a charge per unit of three.five% and rates have since risen to 5%, information technology could be a great move to presume the seller'due south loan.

It's also another incentive the seller can throw into the mix to make their home more bonny to prospective buyers looking for a deal.

Only note that the individual assuming the FHA loan must qualify under the same underwriting guidelines that apply to new loans.

FHA Loan Credit Score Requirements

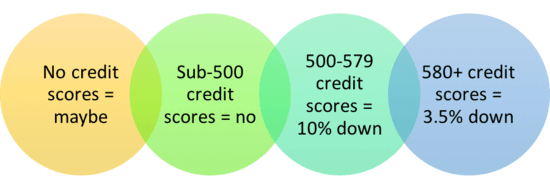

Tin I get an FHA loan with bad credit?

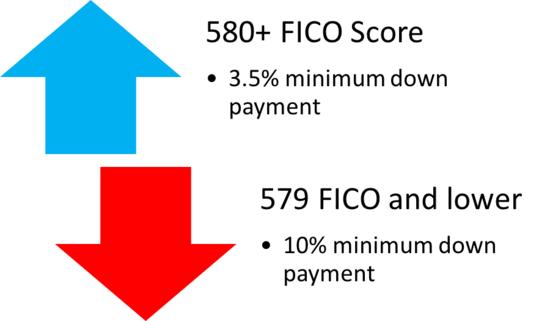

Borrowers with credit scores of 580 and above are eligible for maximum financing, or just three.5% downward. This is the depression-down payment loan program the FHA is famous for.

And a 580 credit score is what I would define every bit "bad," then the answer to that question is yes.

What if my credit score is below 580?

If your credit score is between 500 and 579, your FHA loan is limited to xc% loan-to-value (LTV), meaning you must put down at least x%. This is why you'll probably want to aim higher.

If your credit score is below 500, y'all are non eligible for an FHA loan. All that said, the FHA has some of the most liberal minimum credit scores around.

I tin can't find a lender willing to give me an FHA loan with a 500 credit score.

As noted earlier, these are just FHA guidelines – private banks and mortgage lenders volition likely have higher minimum credit score requirements, so don't be surprised if your 580 FICO score isn't sufficient (at least one lender at present goes as low as 500).

Can I become an FHA loan with no credit score?

Surprisingly, yeah! The FHA makes exceptions for those with non-traditional credit and those with no credit scores whatsoever. You lot can even become maximum financing (3.five% down) as long as you see sure requirements.

The FHA is a little tougher on this type of borrower, imposing lower maximum DTI ratios, requiring two months of cash reserves, and they practice not permit the use of a non-occupant co-borrower.

If y'all have rental history, information technology needs to be clean. If not, you yet need to create a 12-month credit history using Grouping I credit references (rent, utilities, etc.) or Group II references (insurance, tuition, cell telephone, rent-to-ain contracts, child care payments, etc.).

You are allowed no more than one xxx-24-hour interval late on a credit obligation over the past 12 months, and no major derogatory events similar collections/court records filed in the past 12 months (other than medical).

Bold you tin muster all that, it is possible to become an FHA loan without a credit score. Of course, information technology's probably a lot easier if you have a credit score (and a good one at that!).

Since the mortgage crisis struck, FHA loans accept become increasingly popular, essentially replacing subprime lending, largely because of their relatively easy underwriting requirements and government guarantee.

But brand certain yous compare FHA loans with conventional loans too. There volition exist cases when the do good of one outweighs the other. Exist certain to use a payment calculator to factor in all monthly costs.

FHA loans are not guaranteed to be a amend deal than other mortgages, so accept the fourth dimension to store around. And watch out for unscrupulous FHA-qualified lenders who may attempt to misinform you.

Sometimes certain types of loan benefit them more you, so knowing which is best for you earlier yous speak to an interested party might be the all-time way to become.

Are DACA Recipients Eligible for FHA loans?

Yes. After some years of defoliation (and politics), HUD officially announced that effective January 19th, 2021, individuals classified nether the "Deferred Action for Childhood Arrivals" program (DACA) are eligible to apply for mortgages backed by the FHA.

Prior to the announcement (FHA INFO #21-04), in that location was a lot of uncertainty regarding the latter considering the FHA handbook stated, "Non-U.s.a. citizens without lawful residency in the U.Due south. are not eligible for FHA-insured mortgages."

That entire subsection has at present been removed from the handbook to avoid confusion and provide clarity.

The i caveat is that they must likewise exist legally permitted to piece of work in the United states of america, as evidenced past the Employment Potency Document issued by the USCIS

Other than that, you must occupy the property as your primary residence, have a valid Social Security Number (SSN), unless employed by the World Bank, a foreign embassy, or an equivalent employer identified by HUD.

And yous must satisfy the same underwriting requirements, terms, and conditions prepare for U.South. citizens.

Read more: FHA vs. conventional loans

Source: https://www.thetruthaboutmortgage.com/fha-loans/

0 Response to "Qualify for Fha Again After 5 Years"

Post a Comment